There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

Lorem Ipsum is simply dummy text of the printing and typesetting industry.

Sun Oct 5, 2025

1. Introduction

Options trading is one of the most dynamic areas of the financial market, offering opportunities to profit in both bullish and bearish conditions — without direct ownership of the asset.

However, success in this field depends on understanding option pricing principles and market behavior. Concepts like put and call options and critical risk measures — Delta, Vega, and Rho — form the foundation for precision-based decision-making.

Summary:

Exchange-traded options offer liquidity and regulatory oversight, while forward contracts cater to customized but higher-risk arrangements.

Volatility measures the pace of price fluctuation, while Vega indicates how much an option’s price changes with volatility shifts.

Key Insights:

Rising Volatility: Increases option premiums and profit potential.

Vega: Quantifies the impact of volatility on option pricing.

Trade Implication: High volatility offers opportunity but demands disciplined risk control.

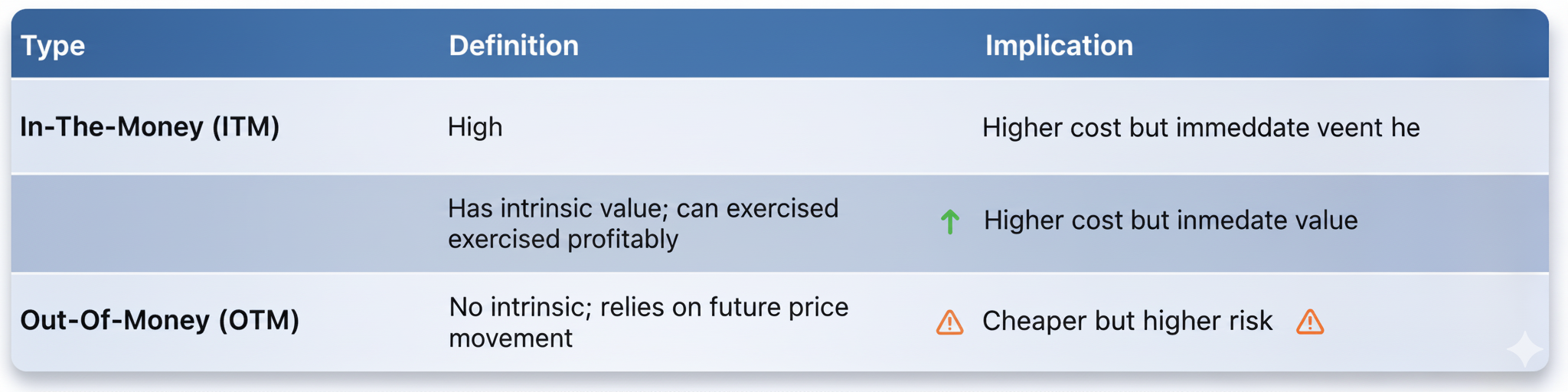

Traders constantly assess whether their options are in or out of the money to make holding or exercising decisions.

A calendar spread involves buying and selling options of the same type but with different expiry dates, leveraging differences in time decay and volatility.

Key Insights:

Near-term Options: Lower premiums (short leg).

Long-term Options: Higher time value (far leg).

Rho Effect:

Rising interest rates → call option premiums increase slightly.

Falling interest rates → put option premiums tend to rise.

Strategic Application:

Understanding Rho enables traders to incorporate macro factors into their portfolio decisions.

Options trading is a multidimensional discipline — blending market analytics, timing precision, and psychological discipline.

By mastering fundamental concepts like puts, calls, Delta, Vega, and Rho, traders transition from speculative participants to strategic operators, capable of identifying value, mitigating risk, and capitalizing on volatility with confidence.

Prof. Sheetal Kunder

SEBI® Research Analyst. Registration No. INH000013800 M.Com, M.Phil, B.Ed, PGDFM, Teaching Diploma (in Accounting & Finance) from Cambridge International Examination, UK. Various NISM Certification Holders. Ex-BSE Institute Faculty. 18 years of extensive experience in Accounting & Finance. Faculty Development Programs and Management Development Programs at the PAN India level to create awareness about the emerging trends in the Indian Capital Market and counsel hundreds of students in career choices in the finance are

Launch your Graphy

Launch your Graphy