There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

To achieve the 60% passing threshold in the NISM Series XIII exam, a candidate must transcend rote memorisation and achieve a profound understanding of the mathematical and logical frameworks that govern derivative pricing and valuation. The curriculum is structured to build knowledge progressively, starting from the foundational definitions of derivatives as contracts that derive value from an underlying asset, such as equity, currency, or interest rates.

Foundational Pricing Models and Equity Dynamics

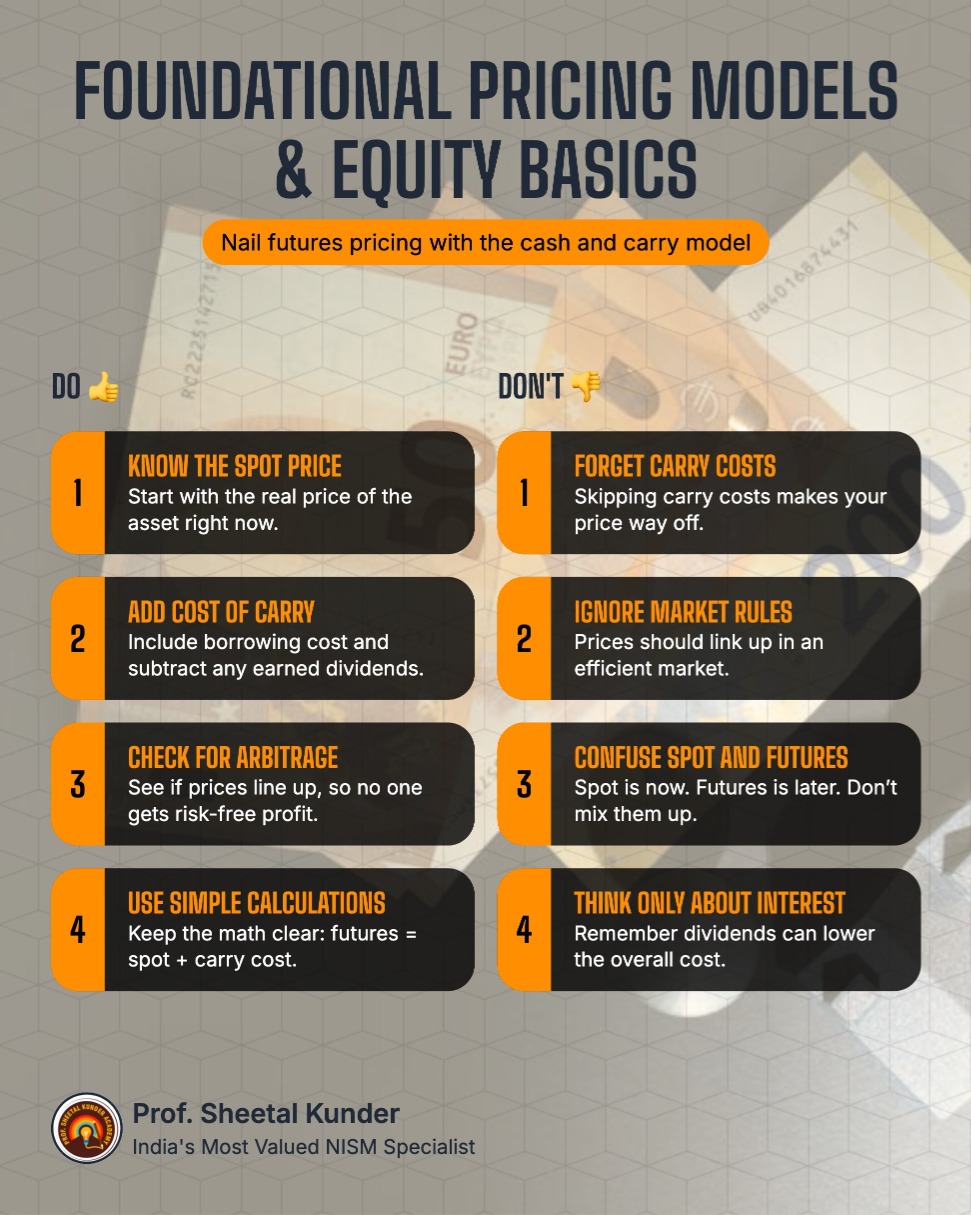

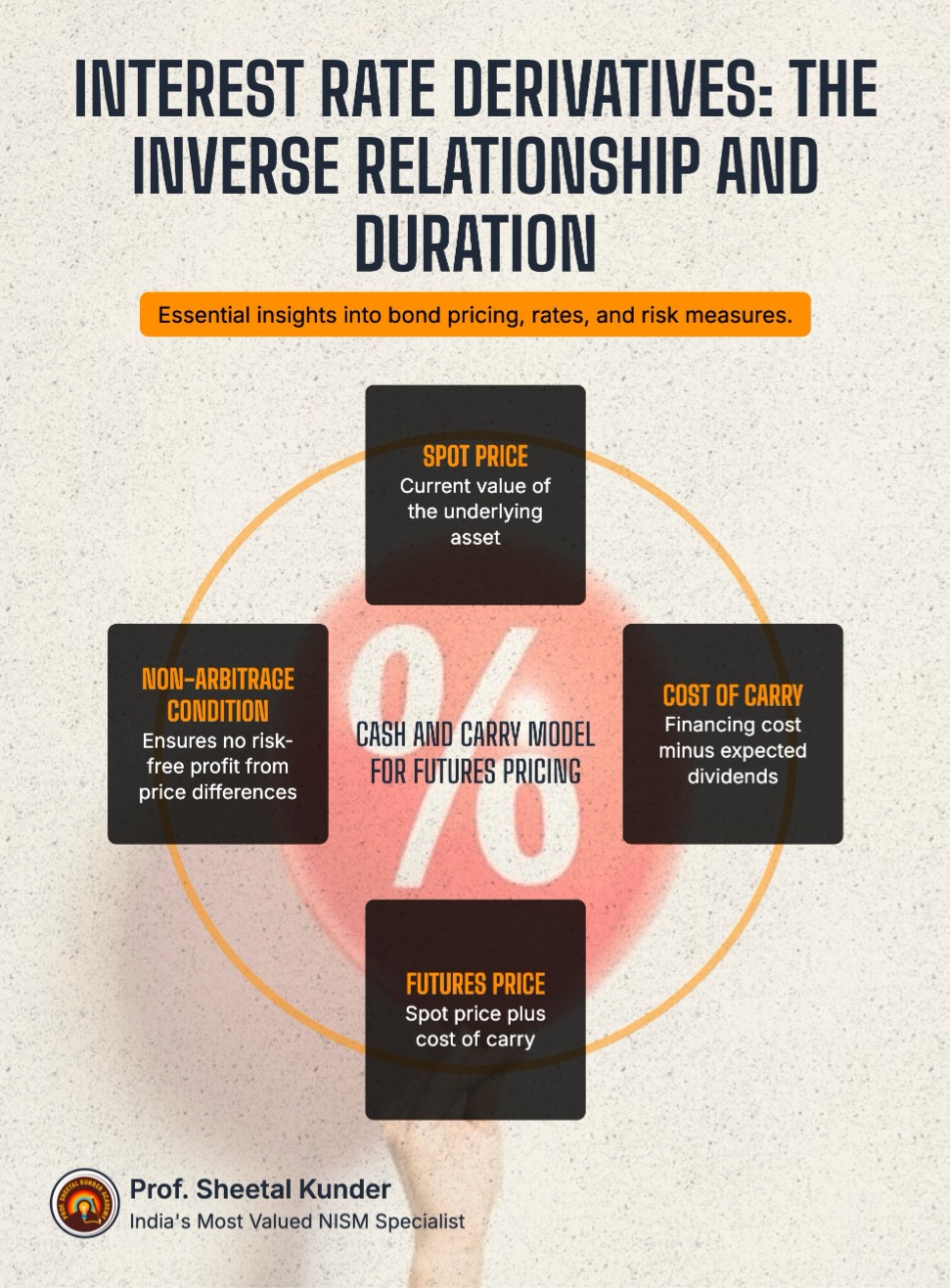

A primary focus of the equity segment is the "Cash and Carry Model" for futures pricing, also known as the non-arbitrage model. This model assumes that in an efficient market, the price of a futures contract equals the spot price plus the "cost of carry"—the financing cost of holding the underlying asset until the delivery date. For financial assets, the cost of carry primarily involves the interest paid to fund the purchase, minus any dividends received during the holding period.

The mathematical representation of this relationship is expressed through LaTeX as:

F = S \times (1 + r - d)^{t}

Where:

Option Greeks and Risk Sensitivity

The curriculum places significant emphasis on "Option Greeks," which are the mathematical measures of an option's sensitivity to various market factors. Mastering these is essential for anyone aiming for a career in risk management or professional trading.

| Greek | Definition and Sensitivity Measure | Formula / Calculation Logic |

| Delta | Sensitivity of the option price to changes in the price of the underlying asset. | \Delta = \frac{\partial V}{\partial S} (Change in Option Price / Unit Change in Underlying) |

| Gamma | Rate of change in Delta for a unit change in the underlying price. | \Gamma = \frac{\partial \Delta}{\partial S} (Change in Delta / Unit Change in Underlying) |

| Theta | Sensitivity of the option price to the passage of time (Time Decay). | \Theta = \frac{\partial V}{\partial t} (Change in Option Price / Change in Time to Expiry) |

| Vega | Sensitivity of option price to changes in market volatility. | \nu = \frac{\partial V}{\partial \sigma} (Change in Option Price / 1% Change in Volatility) |

| Rho | Sensitivity of option price to changes in the risk-free interest rate. | \rho = \frac{\partial V}{\partial r} (Change in Option Price / 1% Change in Interest Rate) |

For SIF managers, Delta management is a critical task. For example, a "Delta Neutral" portfolio is one where the total Delta is zero, meaning the portfolio's value does not change with small movements in the underlying asset's price. This is often achieved through sophisticated hedging strategies that combine futures and options.

Currency Derivatives and the Interest Rate Parity (IRP)

In the currency segment, the pricing of exchange-traded currency futures is governed by the Interest Rate Parity theory. This theory posits that the forward premium or discount for a currency should equal the interest rate differential between the two countries in the currency pair. In the USD-INR context, if Indian interest rates are higher than those in the United States, the USD should trade at a premium in the futures market to prevent arbitrage.

The fundamental unit of change in a currency market is the "Tick Size," the minimum price change allowed. For USD-INR contracts on Indian exchanges, this is typically ₹0.0025. Professionals must also understand the role of the "Bretton Woods" system in historical currency evolution and how modern "Fixed" vs "Floating" rate regimes dictate volatility.

Interest Rate Derivatives: The Inverse Relationship and Duration

Interest Rate Derivatives (IRDs) are often considered the most difficult part of the Series XIII exam because retail participants lack daily practical exposure to them. The core truth of this segment is the "Inverse Relationship": when interest rates rise, the market price of existing fixed-rate bonds falls. This occurs because new bonds will be issued at higher rates, making the older, lower-coupon bonds less attractive.

Key metrics used in IRD include:

Where n is the number of compounding periods per year. For a SIF manager focusing on "Debt Long-Short" strategies, these formulas are not just academic; they are the tools used to position the fund for expected shifts in the RBI's monetary policy.

Prof. Sheetal Kunder

SEBI® Research Analyst. Registration No. INH000013800 M.Com, M.Phil, B.Ed, PGDFM, Teaching Diploma (in Accounting & Finance) from Cambridge International Examination, UK. Various NISM Certification Holders. Ex-BSE Institute Faculty. 18 years of extensive experience in Accounting & Finance. Faculty Development Programs and Management Development Programs at the PAN India level to create awareness about the emerging trends in the Indian Capital Market, and counsel hundreds of students in career choices in the finance area

Launch your Graphy

Launch your Graphy