There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

Is Equity Safe for Senior Understanding Risk the Right Way

{{DATE}}

Retirement marks a phase of transition — from earning to relying on accumulated wealth. Years of saving, investing, and planning finally culminate in a period where the focus shifts from building assets to preserving them.

At this stage, a pressing question emerges: should senior citizens invest in equity? For decades, conventional wisdom has painted equity as a volatile and “unsafe” option for retirees. Fixed deposits, pensions, and government-backed schemes were seen as the only suitable choices.

However, with changing economic conditions, rising life expectancy, and sustained inflation, this mindset is undergoing a transformation. Today, financial experts agree that equity — if allocated judiciously — can play a crucial role in a senior’s investment strategy.

Equity, or ownership in a company, is an asset class that has historically generated superior returns compared to traditional savings instruments. It represents participation in corporate growth — as companies expand and earn profits, shareholders benefit through capital appreciation and dividends. Unlike fixed-income products such as bank deposits or bonds, equity does not offer fixed returns. Its value fluctuates with market conditions. While this volatility deters some investors, it is precisely what gives equity its long-term wealth-building potential.

The Historical Advantage of Equity

Over the past two decades, benchmark indices such as the Nifty 50 have delivered annualized returns of around 11–12%. During the same period, fixed deposits averaged 6–7% before taxes.

Even after accounting for market corrections, equities have consistently outperformed other assets over 10-year or longer horizons. This makes equity a crucial tool for combating inflation and preserving purchasing power — even in retirement.

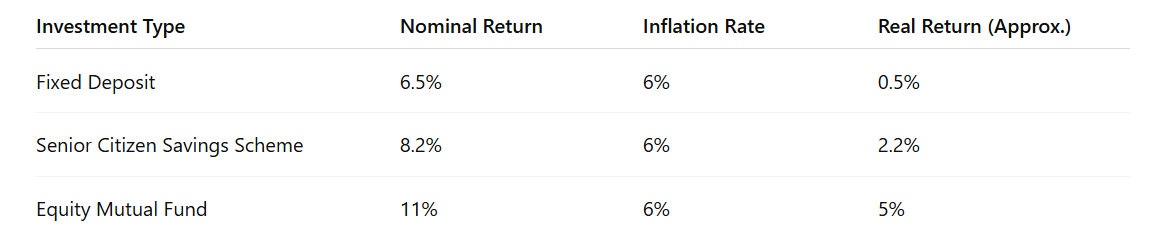

Inflation is the gradual rise in the prices of goods and services. It reduces the value of money and, consequently, the purchasing power of savings.

For example, if your monthly household expenditure is ₹50,000 today and inflation averages 6%, you will need approximately ₹90,000 after 10 years to maintain the same lifestyle. While fixed deposits and government bonds may appear “safe,” their real (inflation-adjusted) returns often lag behind inflation. Consider this comparison:

Traditionally, investors have equated age with risk avoidance. But modern financial planning emphasizes risk capacity and financial independence, not age alone. Risk Capacity vs. Risk Tolerance

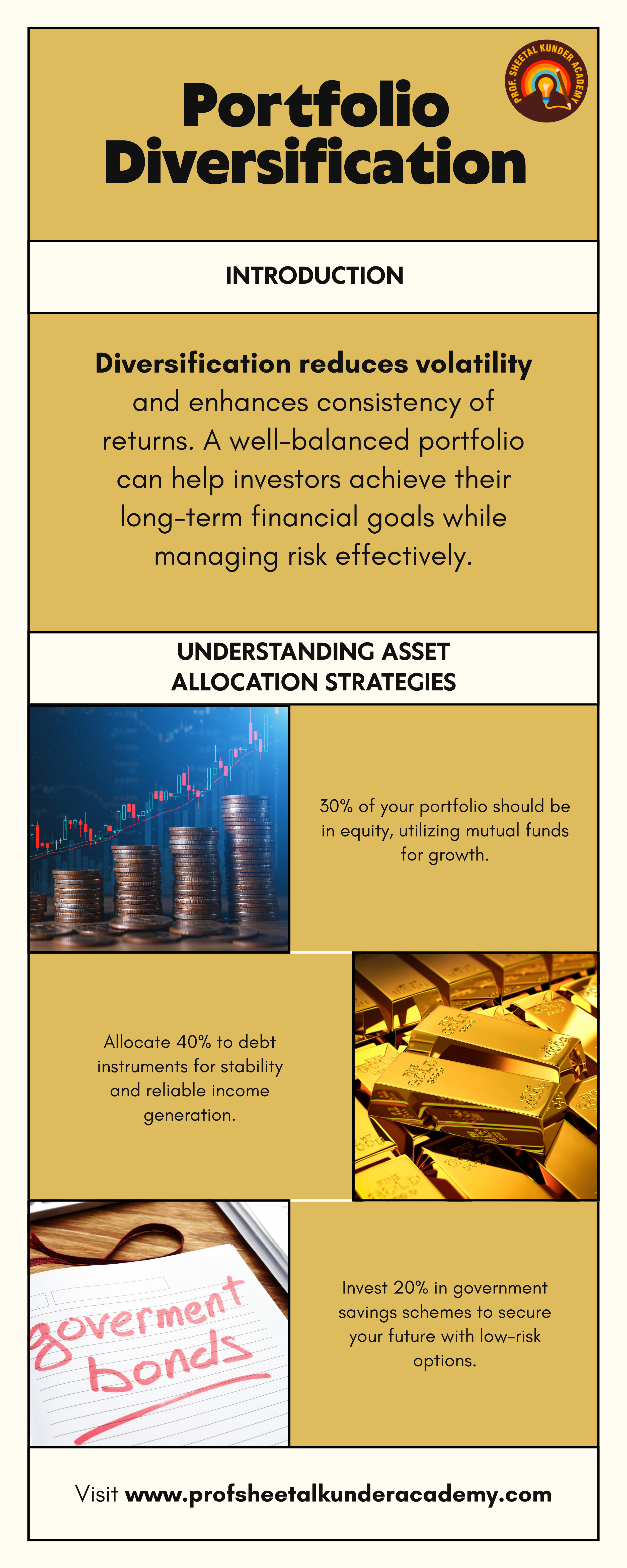

One of the oldest and simplest asset allocation rules is the “100 minus age” formula.

It suggests that your equity exposure should equal 100 minus your age.

For instance:

Senior citizens need not directly invest in shares or track markets daily. There are several professionally managed and relatively stable equity options available:

a) Large-Cap Mutual Funds These funds invest in financially strong, well-established companies. Large caps tend to be less volatile, making them ideal for conservative investors seeking moderate growth.

b) Balanced Advantage (Dynamic Asset Allocation) Funds These funds automatically shift between equity and debt depending on market conditions. When markets rise, they reduce equity exposure; when markets fall, they increase it — ensuring better risk management.

c) Equity Savings Funds These funds blend equity, arbitrage, and debt strategies, generating steady returns of 7–9% with low volatility.

d) Dividend Yield Funds Such funds invest in companies that consistently pay dividends, creating a steady income stream while maintaining growth potential. e) Index Funds or ETFs These track broad indices like the Nifty 50 or Sensex, offering low-cost exposure to diversified equity portfolios.

f) Systematic Withdrawal Plans (SWPs) For retirees who require monthly cash flow, SWPs from mutual funds provide predictable withdrawals while the remaining investment continues to grow.

These instruments enable retirees to participate in market growth without the need for active management or speculation.

6. Importance of Liquidity and Emergency Reserves

Liquidity is the cornerstone of sound retirement planning.

Even the best investment plan can fail if an individual lacks easy access to cash during emergencies. Experts recommend maintaining at least 12 to 18 months of living expenses in liquid instruments such as:

7. The Role of Equity in an Inflationary Environment

India’s average inflation rate over the last two decades has been around 5–6%. Medical inflation, however, is much higher — averaging 8–10% annually.

This means that healthcare costs, which form a significant part of retirement expenses, are rising faster than average inflation. Fixed-income instruments cannot fully offset this escalation. Equity, therefore, acts as a hedge — not because it eliminates inflation, but because it grows faster than inflation over long periods. When used as a partial allocation (20–35%), it ensures that the corpus retains its purchasing power through compounding.

8. When Seniors Should Avoid Equity

While equity offers several advantages, it is not suitable for everyone. Seniors should minimize or avoid it if:

Even with equity exposure, diversification is crucial. A well-diversified portfolio reduces volatility and enhances consistency of returns.

For instance:

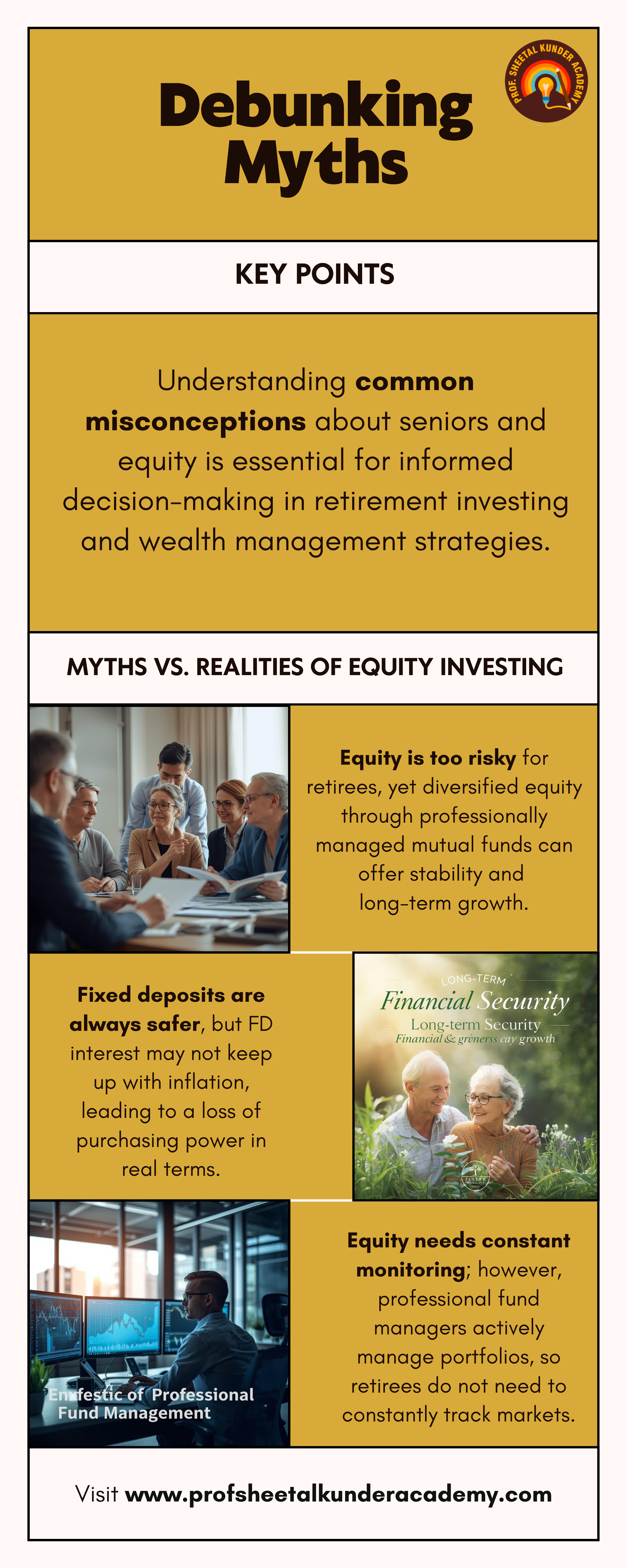

| Myth | Reality |

|---|---|

| “Equity is too risky for retirees.” | Diversified equity via mutual funds can offer stability and long-term growth. |

| “Fixed deposits are always safer.” | FD interest may not beat inflation, leading to loss in real terms. |

| “Equity needs constant monitoring.” | Professional fund managers handle portfolio management for you. |

| “Retirees don’t need growth.” | With rising longevity, even retirees need growth to sustain income for decades. |

Conclusion:

- Equity is not the enemy of senior investors — poor allocation is.

- Completely avoiding equity may appear prudent but often results in slower growth, reduced income sustainability, and diminished purchasing power. A judicious mix of equity and debt, supported by liquidity and disciplined management, can transform retirement portfolios into resilient, income-generating assets. The goal after retirement is not just to preserve money — but to preserve the power of money.

- When used strategically, equity remains a senior investor’s quiet ally against inflation, longevity, and uncertainty.

Key Takeaways

• Equity should form 20–35% of a senior’s portfolio for inflation-adjusted growth.

• Age alone shouldn’t determine risk — financial stability and liquidity should.

Prof. Sheetal Kunder

SEBI® Research Analyst. Registration No. INH000013800 M.Com, M.Phil, B.Ed, PGDFM, Teaching Diploma (in Accounting & Finance) from Cambridge International Examination, UK. Various NISM Certification Holders. Ex-BSE Institute Faculty. 18 years of extensive experience in Accounting & Finance. Faculty Development Programs and Management Development Programs at the PAN India level to create awareness about the emerging trends in the Indian Capital Market and counsel hundreds of students in career choices in the finance area

Launch your Graphy

Launch your Graphy