There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

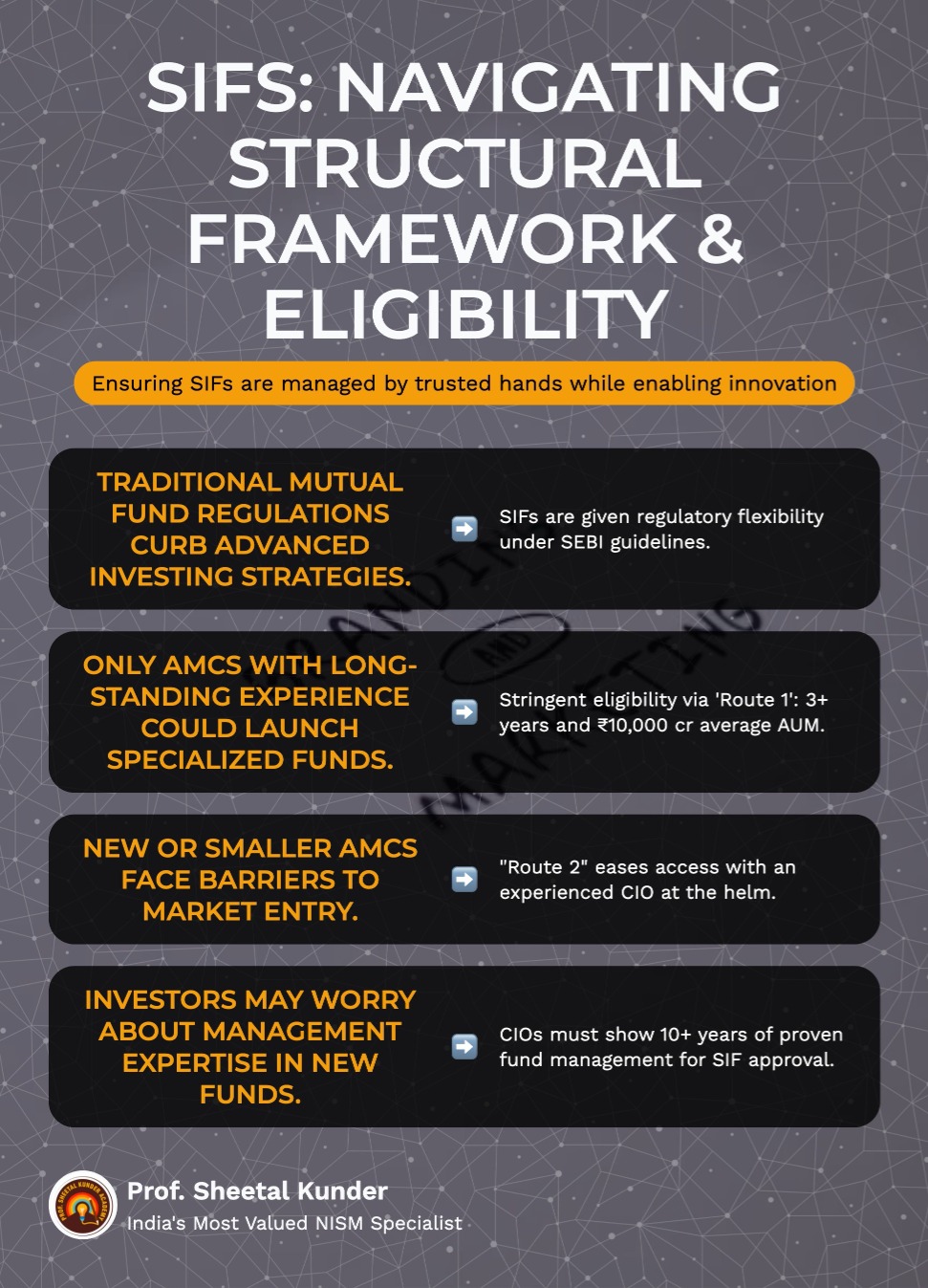

Specialised Investment Funds (SIFs) were introduced by SEBI on April 1, 2025, to provide a structured, flexible vehicle for sophisticated investors. They bridge the gap between traditional mutual funds and high-minimum-threshold products such as Portfolio Management Services (PMS) and Alternative Investment Funds (AIF).

Structural Framework and Eligibility

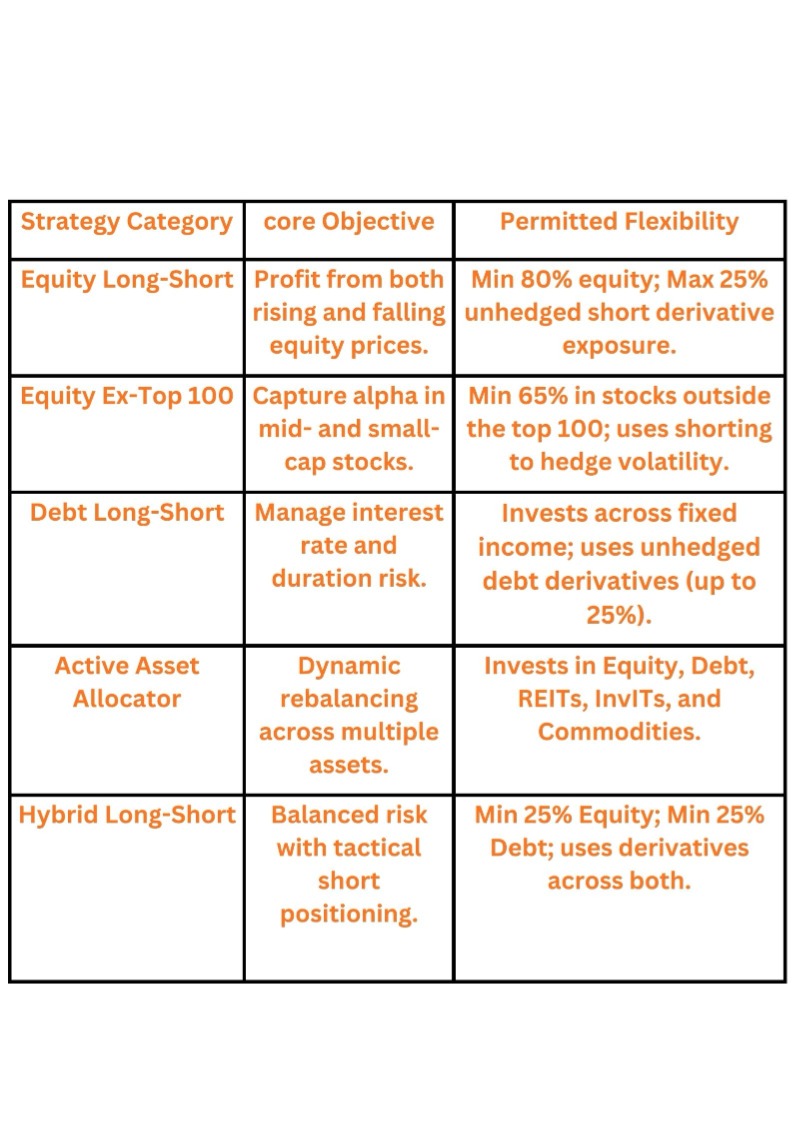

The Power of Long-Short Strategies

The defining feature of SIFs is the ability to take "Short" positions. In a traditional mutual fund, a manager can only profit if the price of a stock goes up. In an SIF, the manager can sell overvalued stocks using derivative instruments (taking a short position) and profit if the price falls. This "Long-Short" approach is designed to provide downside protection. For instance, during a market correction in January 2026, when the Nifty 500 fell by 1.83%, certain SIF strategies reported significantly lower drawdowns, with some falling as little as 0.50%.

This capability is particularly relevant for the "Equity Ex-Top 100" funds. Mid- and small-cap stocks are notoriously volatile, often delivering sharp gains followed by dramatic corrections. By using a long-short strategy, a fund manager can participate in the growth of fundamentally strong mid-caps while simultaneously taking short positions in overvalued sectors, effectively smoothing the return profile for the investor.

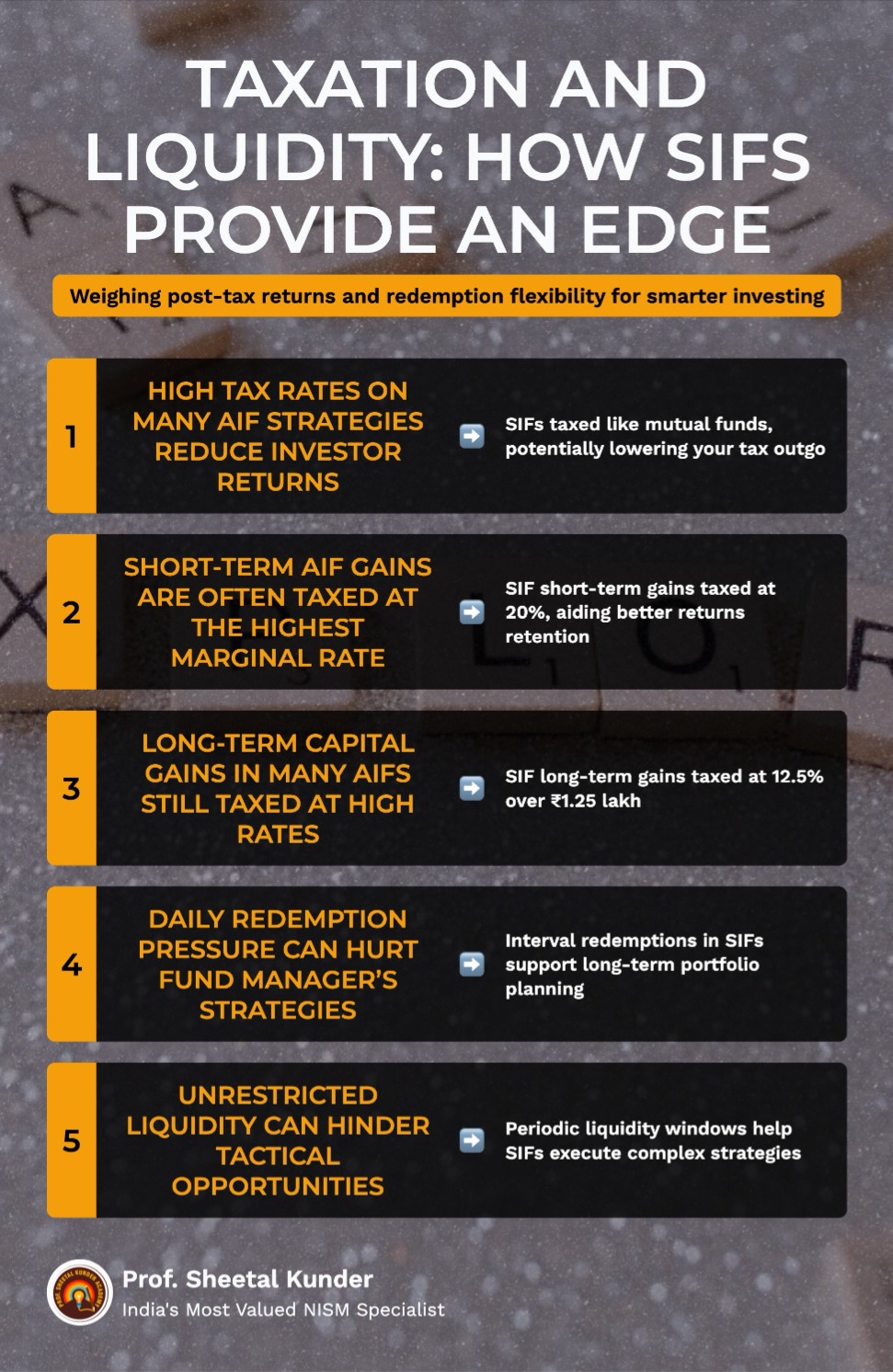

Taxation and Liquidity Considerations

One of the most compelling advantages of SIFs is their tax efficiency compared to AIFs. SIFs enjoy the same taxation status as traditional mutual funds. If a SIF maintains a gross equity exposure of more than 65%, it is classified as an equity fund for tax purposes. This means short-term capital gains (STCG) are taxed at 20%, and long-term capital gains (LTCG) are taxed at 12.5% for gains exceeding ₹1.25 lakh per year. In contrast, many AIF strategies are taxed at the highest marginal rate, which significantly impacts net returns for HNIs.

In terms of liquidity, SIFs are typically structured as "Interval Funds." While traditional funds offer daily redemptions, SIFs may have weekly, fortnightly, or monthly windows, and AMCs can impose notice periods of up to 15 days. This "locked-in" capital allows the fund manager to take long-term tactical calls without worrying about immediate redemption pressure, which is essential for executing complex derivative strategies.

The Role of the NISM XIII Certified Distributor

The sophistication of SIFs makes the role of the distributor paramount. SEBI's mandate that SIF distributors must pass the NISM Series XIII exam ensures that these products are not "mis-sold" as regular mutual funds. A certified distributor must be able to explain the "Risk-band" level of the SIF, which ranges from Level 1 (Lowest Risk) to Level 5 (Highest Risk). They must also help the investor understand that SIFs are "strategy-driven" and require a longer investment horizon, typically aligned with market cycles rather than short-term fluctuations.

Launch your Graphy

Launch your Graphy