There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

{{DATE}}

Over the last decade, India’s capital markets have witnessed rapid growth in participation, especially in derivatives such as Futures & Options (F&O). While increased participation reflects growing financial awareness, it has also exposed a critical weakness in the ecosystem—lack of structured knowledge among retail participants and intermediaries.

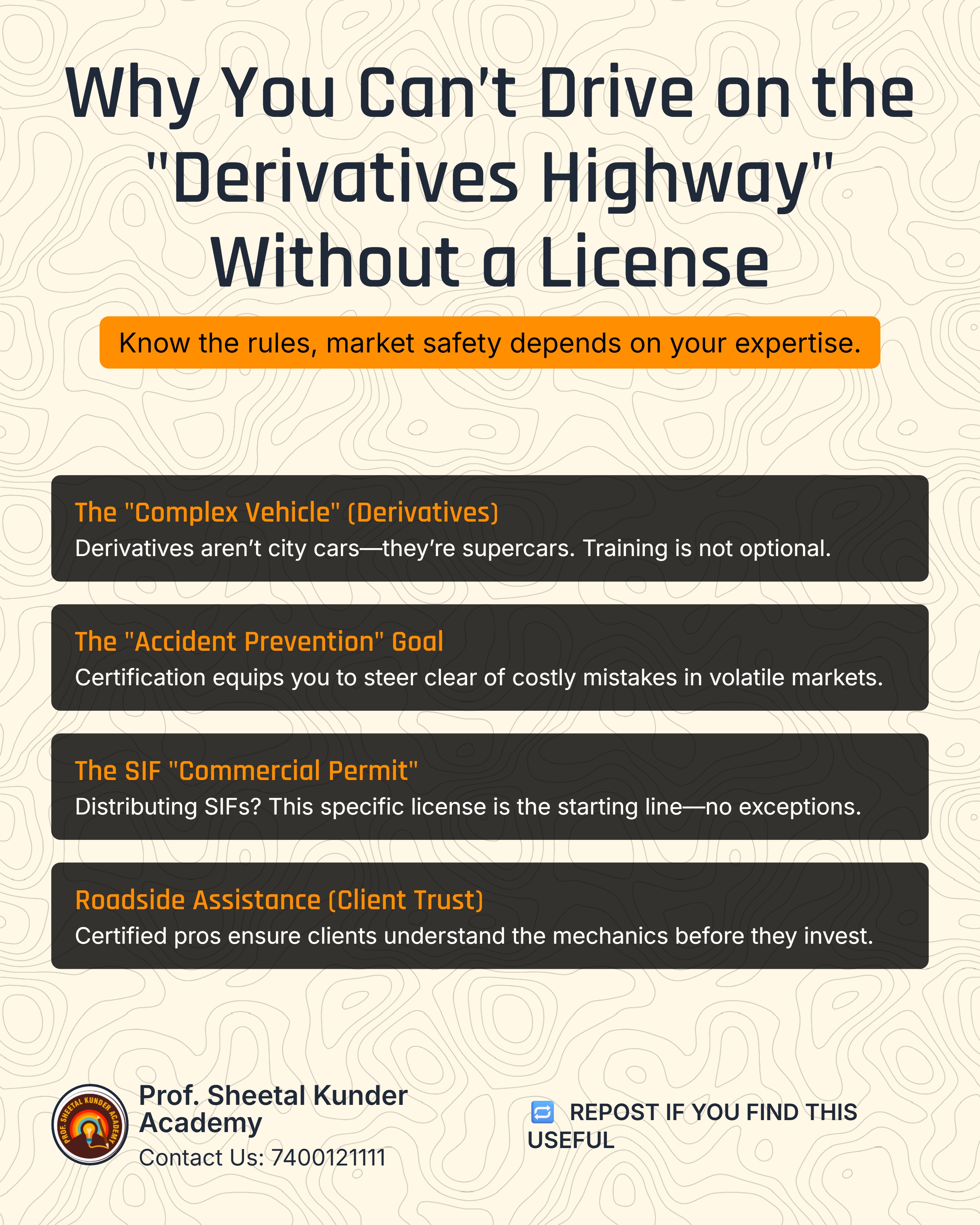

The NISM Series XIII – Common Derivatives Certification was introduced by SEBI not as an academic formality, but as a regulatory safeguard. As discussed in the detailed conversation between Prof. Sheetal Kunder and Nitin Manapure, this certification plays a pivotal role in ensuring that derivatives-linked products, especially Structured Investment Funds (SIFs), are distributed responsibly.

This blog explores why SEBI made NISM Series XIII mandatory, the market realities that led to this decision, and how the certification strengthens investor protection, professional accountability, and long-term market stability.

India has one of the largest retail participation bases in F&O trading globally. However, data consistently shows that a majority of retail traders incur losses.

As highlighted in the discussion:

Retail investors lose tens of thousands of crores annually

Losses are concentrated among under-informed participants

Derivatives trading has become speculative rather than strategic

Derivatives are inherently zero-sum instruments—when one party loses, another gains.

Retail losses are often offset by gains made by:

Large institutional investors

Foreign Institutional Investors (FIIs)

Global financial institutions

These entities have:

Advanced systems

Professional risk management

Structured strategies

This asymmetry created a pressing regulatory concern.

It is important to clarify what SEBI does not intend:

SEBI does not aim to stop derivatives trading

SEBI does not guarantee profits

SEBI does not restrict innovation

Instead, SEBI focuses on frameworks, safeguards, and accountability.

SEBI’s responsibilities include:

Investor protection

Market integrity

Fair practices

Intermediary regulation

Mandatory certification is a natural extension of this mandate.

Unlike traditional mutual funds, derivatives involve:

Leverage

Volatility

Non-linear payoffs

Complex risk dynamics

Selling or advising on derivatives without understanding these aspects leads to mis-selling and investor harm.

Many mutual fund distributors:

Have strong product knowledge in equity and debt

Lack exposure to derivatives mechanics

Are unfamiliar with currency and interest rate markets

NISM Series XIII bridges this gap.

Structured Investment Funds introduced:

Derivatives-based strategies

Multi-asset exposure

Advanced risk management

This made certification non-negotiable for distributors.

SIFs cannot be sold using:

Relationship trust alone

Past mutual fund experience

Generic return narratives

They require technical explanation and risk disclosure, which certification ensures.

NISM Series XIII covers:

Equity derivatives

Currency derivatives

Interest rate derivatives

This holistic coverage ensures that professionals understand the entire derivatives ecosystem, not just equity F&O.

As emphasized in the discussion:

The exam is concept-driven

Questions are application-based

Memorization does not work

This aligns with SEBI’s goal of knowledge-based regulation.

Mandatory certification:

Filters out unprepared intermediaries

Encourages serious professionals

Raises industry standards

This benefits both investors and ethical distributors.

Certified professionals are better equipped to:

Explain risks clearly

Set realistic expectations

Avoid exaggerated claims

This reduces disputes and regulatory issues.

While investor awareness is improving:

Product complexity is increasing faster

Retail investors still rely on intermediaries

SEBI focuses on educating intermediaries, who then educate investors.

Certification creates accountability:

Professionals are responsible for advice

Misrepresentation carries consequences

Ethical standards are enforced

This strengthens trust in the system.

Distributors are now expected to:

Upgrade technical skills

Understand derivatives logic

Explain structured products confidently

This marks a shift from volume-based distribution to knowledge-based advisory.

Certification provides:

Higher credibility

Competitive differentiation

Access to new product categories

Professionals who adapt early gain long-term advantages.

As discussed in the podcast:

30–40 days of structured preparation is sufficient

The exam tests basics, not advanced trading

A 60% score is achievable with concept clarity

Fear often comes from misinformation, not reality.

The driving license analogy is crucial:

A license does not make you an expert driver

It ensures you understand rules and safety

Similarly, NISM XIII ensures minimum professional competence.

SEBI could have:

Restricted retail participation

Banned certain products

Raised investment thresholds

Instead, it chose education and certification, reflecting a progressive regulatory approach.

Globally:

Derivatives distribution requires certification

Intermediaries are heavily regulated

Investor protection is paramount

NISM Series XIII aligns India with these standards.

A qualified intermediary ecosystem:

Builds investor confidence

Encourages responsible innovation

Reduces systemic risk

This supports sustainable market expansion.

Going forward:

More advanced certifications may emerge

Product complexity will increase

Regulatory expectations will rise

NISM Series XIII is the foundation, not the endpoint.

SEBI’s decision to make NISM Series XIII mandatory is rooted in practical market realities, not theoretical compliance. Rising retail losses, complex derivative products, and the introduction of Structured Investment Funds demanded a knowledge-first regulatory approach.

Mandatory certification:

Protects investors

Disciplines the market

Elevates professional standards

Enables responsible innovation

As emphasized in the discussion, NISM Series XIII is not a hurdle—it is a license to operate responsibly in India’s evolving derivatives ecosystem.

Prof. Sheetal Kunder

Launch your Graphy

Launch your Graphy